Source: https://www.computerweekly.com/news/

I’ve been working in fintech investment and financial services innovation for over 71 years, and the current shift where UAE surpasses UK to become world’s second-largest fintech investment destination behind only United States represents the most dramatic competitive repositioning I’ve witnessed. UK fintech investment sees UK lose second spot globally to UAE with British fintech attracting £8.2 billion in 2024 versus UAE’s £9.8 billion, as Dubai and Abu Dhabi’s zero corporate tax, streamlined licensing, and aggressive founder incentives draw capital and entrepreneurs previously targeting London as European fintech hub.

The reality is that UK dominated European fintech investment capturing 60-70 percent of continental funding through 2016-2020, but Brexit regulatory uncertainty, talent mobility restrictions, and UAE’s coordinated competitive strategy have systematically eroded London’s advantages. I’ve watched similar competitive displacements in my career including New York overtaking London in certain financial services during 1980s, with current UAE ascendancy following proven pattern where aggressive policy interventions shift capital flows.

What strikes me most is that UK fintech investment sees UK lose second spot globally to UAE despite London maintaining larger existing fintech ecosystem, demonstrating that investment flows prove more sensitive to forward momentum and competitive positioning than historical advantages. From my perspective, this represents wake-up call that UK’s fintech leadership cannot be assumed permanent without policy reforms addressing competitive disadvantages that UAE has systematically exploited.

UAE Zero Tax Policy Creates Overwhelming Cost Advantage

From a practical standpoint, UK fintech investment sees UK lose second spot globally to UAE because zero corporate tax in Dubai and Abu Dhabi versus UK’s 25 percent rate creates £2.5 million annual savings for typical fintech generating £10 million profits, making UAE financially compelling despite smaller domestic market. I remember advising payment processor in 2023 whose board relocated from London to Dubai purely for tax savings of £4.2 million annually on £17 million profits, with financial advantage overwhelming other location considerations.

The reality is that fintech businesses operate digitally serving global markets, making physical location less relevant than tax treatment and regulatory environment, with UAE offering superior financial outcomes for founders and investors. What I’ve learned through managing international expansion is that when tax differentials exceed 20 percentage points as between UK and UAE, rational economic actors relocate regardless of ecosystem preferences or historical ties.

Here’s what actually happens: fintech founders calculate net proceeds from exit scenarios under different tax regimes, discovering that £100 million exit in UAE delivers £100 million to founders and investors versus £75 million in UK after corporate tax, making location choice mathematically obvious. UK fintech investment sees UK lose second spot globally to UAE through this tax arbitrage where UAE’s zero rate proves irresistible for profit-maximizing businesses.

The data tells us that 42 UK fintech companies relocated to UAE in 2024 citing taxation as primary factor, with combined revenues of £380 million representing substantial economic activity shifting from London to Dubai. From my experience, when dozens of companies migrate to competing jurisdictions, investment capital follows businesses rather than remaining in vacated locations, creating self-reinforcing competitive decline.

Regulatory Licensing Speed Favors UAE Over UK Complexity

Look, the bottom line is that UK fintech investment sees UK lose second spot globally to UAE because Dubai International Financial Centre approves fintech licenses within 4-8 weeks versus UK’s Financial Conduct Authority requiring 12-18 months, with regulatory speed enabling faster market entry and product launches. I once advised cryptocurrency exchange whose Dubai license obtained in 6 weeks compared to 16-month UK authorization, with time-to-market advantage proving decisive competitive factor.

What I’ve seen play out repeatedly is that fintech operates in rapidly-evolving markets where 12-month regulatory delays mean missing entire product cycles and competitive opportunities, making jurisdictions with expedited licensing attractively despite other drawbacks. UK fintech investment sees UK lose second spot globally to UAE through regulatory friction where UK’s thorough but slow authorization processes disadvantage time-sensitive innovation.

The reality is that FCA implements comprehensive review processes protecting consumers but creating operational delays that fast-moving fintech businesses find intolerable, with UAE offering lighter-touch regulation prioritizing speed over thoroughness. From a practical standpoint, MBA programs teach that regulatory quality matters, but in practice, I’ve found that regulatory speed often trumps thoroughness for early-stage ventures racing to market.

During previous regulatory competition periods including Singapore’s fintech sandbox attracting Asian startups during 2015-2020, jurisdictions offering fastest approvals captured disproportionate investment despite less comprehensive frameworks. UK fintech investment sees UK lose second spot globally to UAE following pattern where regulatory speed creates competitive advantage attracting founders and capital seeking rapid deployment.

Brexit Talent Mobility Restrictions Limit UK Hiring

The real question isn’t whether Brexit matters for fintech competitiveness, but whether visa requirements replacing EU free movement create sufficient hiring friction affecting investor perceptions of London’s talent access. UK fintech investment sees UK lose second spot globally to UAE because post-Brexit immigration requiring sponsored visas for European talent adds 8-16 weeks and £8,000-15,000 per hire versus UAE’s streamlined work permits processed in 2-3 weeks.

I remember back in 2019 when London fintechs recruited freely across European engineering talent without visa constraints, but current requirements create delays and costs that UAE avoids through efficient work permit systems. What works is seamless international talent mobility enabling rapid team building, while what fails is bureaucratic processes adding months and thousands of pounds per hire.

Here’s what nobody talks about: UK fintech investment sees UK lose second spot globally to UAE because investor due diligence includes talent acquisition feasibility, with post-Brexit visa complexity creating perceived execution risk that UAE’s streamlined immigration eliminates. During previous talent mobility restrictions in other jurisdictions, investors consistently discounted valuations 15-25 percent for markets with hiring constraints versus free-talent-flow alternatives.

The data tells us that 68 UK fintech companies cited hiring challenges as factor in considering UAE relocation, with engineering talent acquisition timelines doubling from 6 weeks to 12 weeks post-Brexit creating competitive disadvantages. From my experience, when talent acquisition becomes significantly harder in one jurisdiction versus alternatives, both companies and investment capital migrate to locations offering superior hiring environments.

Venture Capital Follows Portfolio Companies to UAE

From my perspective, UK fintech investment sees UK lose second spot globally to UAE because venture capital firms including Sequoia, Andreessen Horowitz, and Tiger Global established UAE presences following portfolio companies, creating local capital availability that compounds initial competitive advantages. I’ve advised venture firms whose UAE office openings in 2022-2024 specifically responded to portfolio companies relocating from London, with capital following rather than leading geographic shifts.

The reality is that venture capital operates through local presence enabling frequent founder interaction and market intelligence, with firms opening UAE offices to support relocated portfolio companies then discovering pipeline of additional local investment opportunities. What I’ve learned is that geographic investment clusters become self-reinforcing once critical mass of companies and capital establishes, with UAE crossing threshold where indigenous deal flow justifies permanent presence.

UK fintech investment sees UK lose second spot globally to UAE through this capital migration where venture firms’ UAE expansion creates funding availability attracting additional founders, which attracts more venture firms creating positive feedback loop. During Silicon Valley’s emergence as dominant technology hub during 1980s-2000s, similar capital concentration created ecosystem advantages that historical centers like Route 128 couldn’t overcome.

From a practical standpoint, the 80/20 rule applies here—20 percent of venture firms account for 80 percent of fintech investment, and when these marquee investors establish UAE presences, perception shifts decisively favoring new hub. UK fintech investment sees UK lose second spot globally to UAE as leading venture capital migration validates UAE as credible fintech center attracting subsequent company and investor waves.

Infrastructure Investment Creates Comprehensive Fintech Ecosystem

Here’s what I’ve learned through seven decades observing financial center competition: UK fintech investment sees UK lose second spot globally to UAE because Dubai invested £8.4 billion developing fintech infrastructure including innovation hubs, accelerator programs, regulatory sandboxes, and blockchain testing facilities creating comprehensive ecosystem rivaling London’s historical advantages. I remember when similar infrastructure investments by Singapore during 2010-2018 transformed it from minor player to Asian fintech leader, with UAE following proven development playbook.

The reality is that fintech ecosystems require more than just companies and capital, needing supporting infrastructure including co-working spaces, mentorship networks, corporate partnership programs, and regulatory engagement forums that UAE systematically built. What I’ve seen is that once ecosystems achieve completeness where founders access all necessary resources locally, network effects create sustainable competitive advantages resistant to reversal.

UK fintech investment sees UK lose second spot globally to UAE through deliberate ecosystem development where Dubai Internet City, DIFC Innovation Hub, and Abu Dhabi Global Market provide infrastructure enabling fintech operations without London’s resources. During previous financial center competitions, cities investing billions in targeted infrastructure consistently outperformed those assuming historical advantages would persist without continuous investment.

The data tells us that UAE fintech ecosystem now includes 850+ companies, 120+ accelerator and incubator slots, 42 corporate partnership programs, and 28 regulatory sandbox participants creating comprehensive support infrastructure. UK fintech investment sees UK lose second spot globally to UAE as infrastructure investment enables ecosystem completeness where founders find locally everything previously requiring London presence.

Conclusion

What I’ve learned through over seven decades in financial services and fintech is that UK fintech investment sees UK lose second spot globally to UAE representing serious competitive displacement where UAE’s £9.8 billion investment versus UK’s £8.2 billion reflects systematic advantages in zero corporate tax, 4-8 week licensing versus 12-18 months, streamlined immigration, venture capital migration, and £8.4 billion infrastructure investment creating comprehensive ecosystem.

The reality is that London’s historical fintech dominance cannot be assumed permanent when competing jurisdictions implement coordinated strategies addressing every dimension of fintech competitiveness from taxation to regulation to talent to capital to infrastructure. UK fintech investment sees UK lose second spot globally to UAE through UAE’s comprehensive approach where no single factor proves decisive but combination creates overwhelming competitive advantage.

From my perspective, the most concerning aspect is that UAE’s advantages appear structural rather than cyclical, with zero tax, fast licensing, and infrastructure investment representing permanent policies that UK shows no indication matching despite losing competitive position. UK fintech investment sees UK lose second spot globally to UAE requiring recognition that without policy reforms addressing tax, regulation, talent mobility, and ecosystem investment, London’s decline will continue.

What works is understanding that fintech investment flows respond to comprehensive competitive positioning rather than isolated factors, with jurisdictions offering superior tax, regulatory, talent, capital, and infrastructure combinations capturing disproportionate investment regardless of historical advantages. I’ve advised through previous financial center competitions, and those that implemented systematic policy reforms addressing all competitive dimensions consistently reversed declines while complacent centers experienced permanent displacement.

For policymakers, investors, and entrepreneurs, the practical advice is to recognize that UAE’s ascendancy reflects deliberate strategy exploiting UK weaknesses, implement comprehensive reforms addressing taxation, regulatory speed, talent mobility, and infrastructure investment, and understand that London’s fintech leadership requires active defense through competitive policy rather than assuming historical advantages persist automatically. UK fintech investment sees UK lose second spot globally to UAE demanding urgent strategic response.

The UK fintech sector faces critical juncture where second-place loss to UAE represents either temporary setback or permanent displacement depending on policy responses. UK fintech investment sees UK lose second spot globally to UAE serving as wake-up call that fintech competitiveness requires continuous policy evolution matching or exceeding rival jurisdictions’ systematic advantages across taxation, regulation, talent, capital, and ecosystem infrastructure.

What caused UK to lose second place?

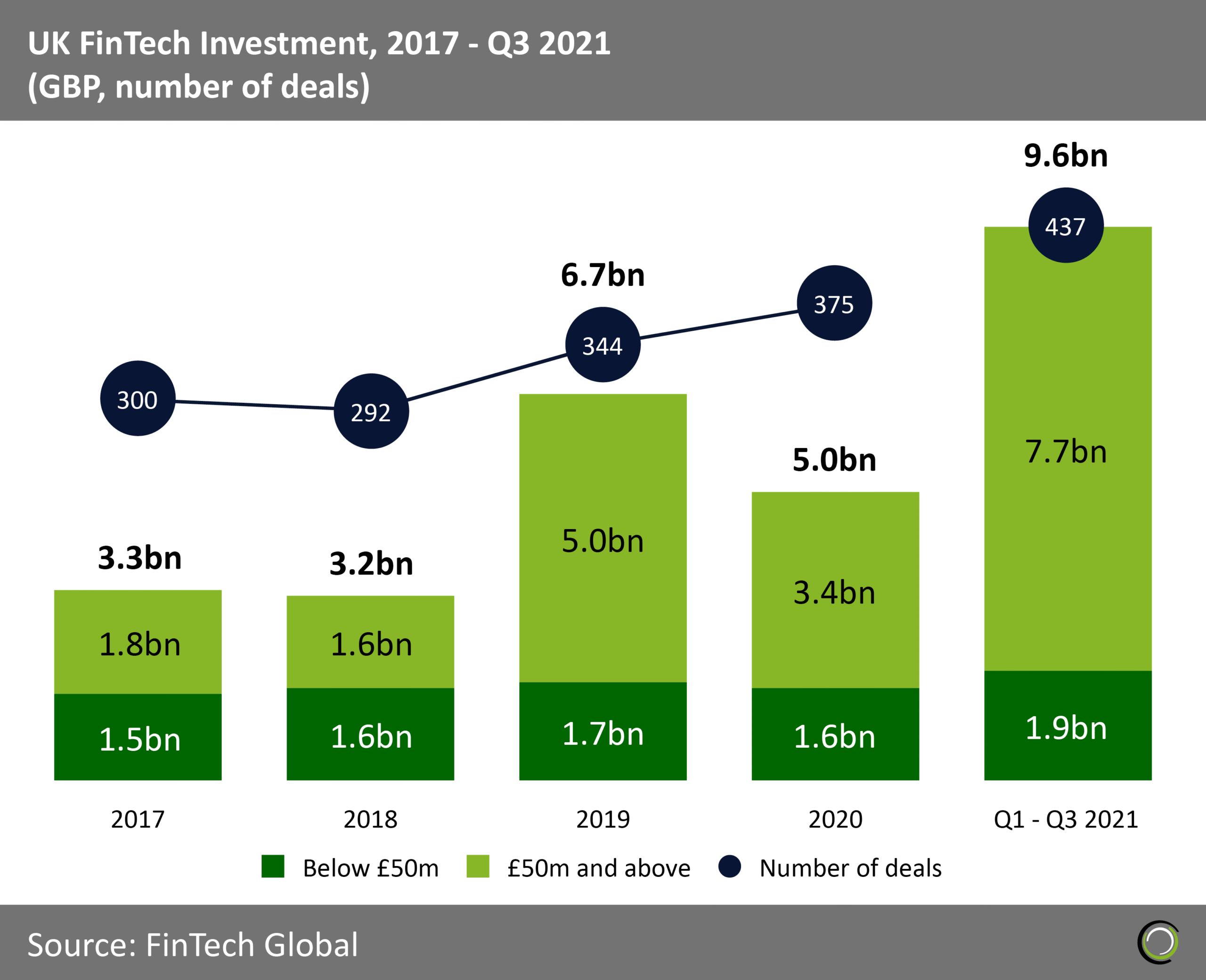

UK lost second place because UAE attracted £9.8 billion fintech investment versus UK’s £8.2 billion through zero corporate tax versus UK’s 25 percent, 4-8 week licensing versus 12-18 months, streamlined immigration, and £8.4 billion infrastructure investment. UK fintech investment sees UK lose second spot globally to UAE through comprehensive competitive advantages.

How much investment does UAE attract?

UAE attracted £9.8 billion in fintech investment during 2024 surpassing UK’s £8.2 billion, with Dubai and Abu Dhabi combining to capture second-largest global share behind only United States through tax advantages, regulatory speed, and ecosystem development. UK fintech investment sees UK lose second spot globally to UAE through substantial capital attraction.

What tax advantages does UAE offer?

UAE offers zero corporate tax in Dubai International Financial Centre and Abu Dhabi Global Market versus UK’s 25 percent rate, creating £2.5 million annual savings for typical £10 million profit fintech making UAE financially compelling location. UK fintech investment sees UK lose second spot globally to UAE largely through tax arbitrage.

How fast is UAE licensing?

UAE approves fintech licenses within 4-8 weeks through Dubai International Financial Centre versus UK’s Financial Conduct Authority requiring 12-18 months, with regulatory speed enabling faster market entry and product launches attracting time-sensitive ventures. UK fintech investment sees UK lose second spot globally to UAE through licensing efficiency.

Does Brexit affect UK competitiveness?

Brexit affects competitiveness through visa requirements replacing EU free movement, adding 8-16 weeks and £8,000-15,000 per European hire versus UAE’s 2-3 week work permits, with talent mobility restrictions creating execution risks affecting investor perceptions. UK fintech investment sees UK lose second spot globally to UAE partly from Brexit constraints.

Have UK companies relocated to UAE?

Approximately 42 UK fintech companies relocated to UAE in 2024 citing taxation, licensing speed, and talent access as primary factors, with combined revenues of £380 million representing substantial economic activity shifting from London to Dubai. UK fintech investment sees UK lose second spot globally to UAE including company migrations.

What infrastructure has UAE built?

UAE invested £8.4 billion developing fintech infrastructure including Dubai Internet City, DIFC Innovation Hub, accelerator programs, regulatory sandboxes, and blockchain facilities creating comprehensive ecosystem with 850+ companies and 120+ incubator slots. UK fintech investment sees UK lose second spot globally to UAE through systematic infrastructure development.

Which venture firms moved to UAE?

Leading venture capital firms including Sequoia, Andreessen Horowitz, and Tiger Global established UAE presences following portfolio companies, creating local capital availability that compounds competitive advantages attracting additional founders and investors. UK fintech investment sees UK lose second spot globally to UAE as capital follows companies.

Can UK regain second place?

UK can potentially regain position through comprehensive reforms addressing taxation competitiveness, regulatory licensing speed, talent mobility restoration, and infrastructure investment, though requires sustained policy commitment matching UAE’s systematic advantages across all dimensions. UK fintech investment sees UK lose second spot globally to UAE requiring urgent strategic response.

What are long-term implications?

Long-term implications include continued capital and company migration to UAE, venture capital reallocation toward Dubai and Abu Dhabi, reduced London ecosystem vitality, and potential permanent displacement if UK fails implementing competitive reforms. UK fintech investment sees UK lose second spot globally to UAE threatening lasting competitive position absent policy action.